.png)

On May 12, 2026, the Depository Trust & Clearing Corporation, the entity that sits underneath nearly all of America’s securities markets, announced that its Collateral AppChain platform would integrate Chainlink CRE and relevant data standards to power pricing, valuation, margining, collateral optimization, and settlement. The platform is targeting a Q4 2026 production launch, with further development planned afterward.

DTCC processed about $4.7 quadrillion in securities transactions in 2025, held custody of securities from more than 150 countries valued at $114 trillion, and processed more than 25 billion trade messages during the year. It’s effective at handling most financial operations, except collateral, and Chainlink seems to be the key to solving that problem. For Chainlink, DTCC’s AppChain is a major opportunity to enter the top tier of financial infrastructure providers as an institutional-grade data and infrastructure provider.

The Problem with Collateral in Finance

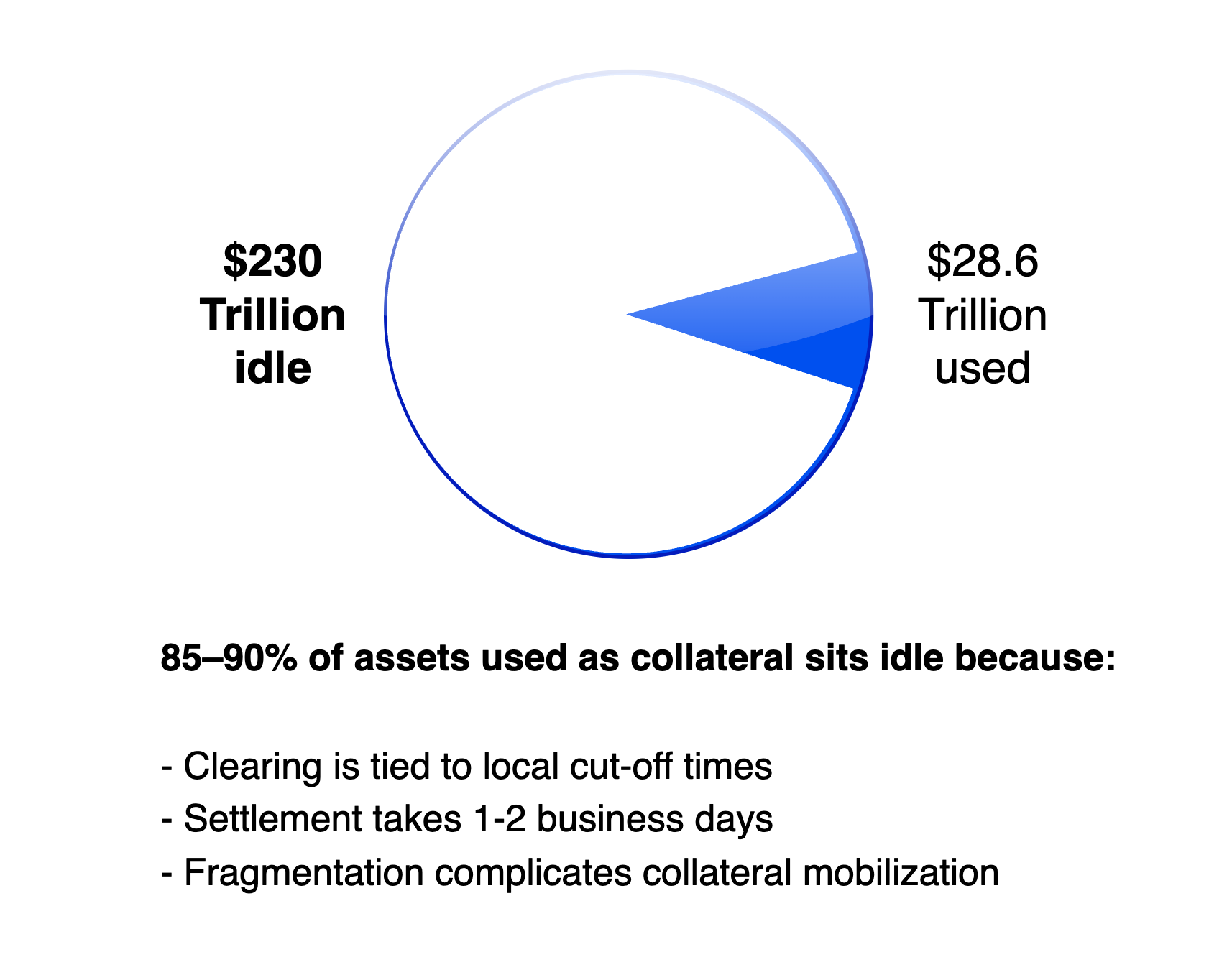

According to the World Economic Forum’s analysis, there are $255 trillion in marketable securities available for use as collateral globally, but only $28.6 trillion are actively being used. The vast majority — 85-90% — of eligible collateral in the global financial system sits idle because the infrastructure was built for a slower financial system and has remained largely unchanged for decades.

First, the infrastructure for moving collateral still relies on daily cut-off times. Currency transactions can be cleared only when the corresponding banks are open, creating strict windows for moving EUR, GBP, USD, JPY, and other currencies. Miss the window? Wait another 16-18 hours for the next one.

Second, the infrastructure was designed around T+2 settlement. Most collateral-related transactions executed today are legally settled only two days later because some parts of the process are still not automated, and humans need time to complete them correctly.

Third, collateral is fragmented across many institutions. A large global institution may hold bonds with a dozen different custodians, across half a dozen jurisdictions, each operating under different CSD rules, different cut-off times, different eligibility standards, and different netting arrangements. Moving those assets as a whole requires serious coordination among many intermediaries.

These three major issues lead to overcollateralization. Firms pledge more collateral than necessary to absorb unexpected events without triggering liquidations or fines: timing gaps, pricing uncertainty, “failed to receive” errors, margin calls, and more.

That’s what causes at least part of the 90% of eligible collateral to simply sit idle.

How Tokenization Can Fix The Problems With Collateral

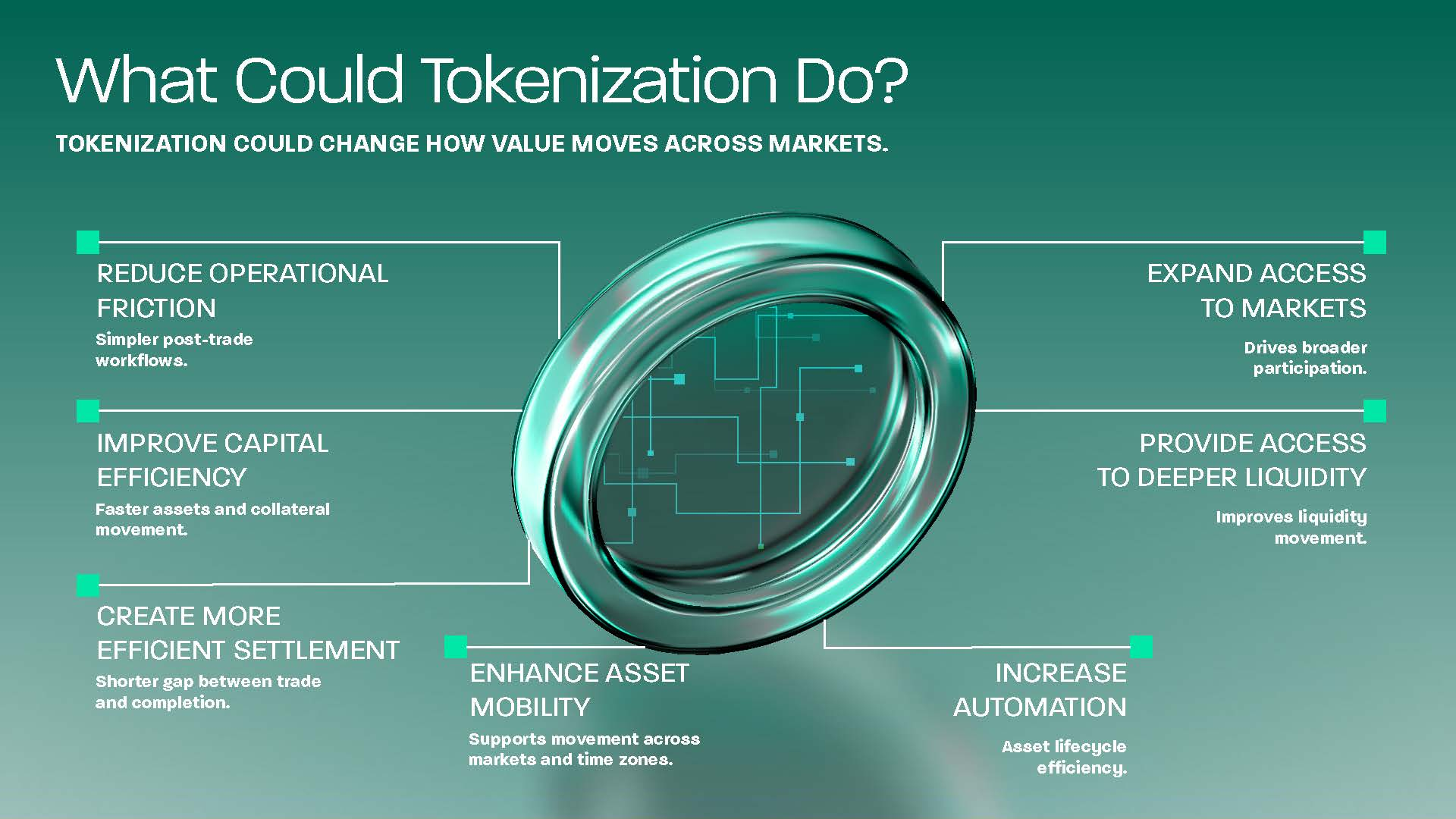

DTCC’s thesis is that a tokenized representation of a collateral asset is easier to transfer, track, value, and automate than the underlying asset itself.

For example, a bank holds $100M in Treasury bills. It needs to use them as collateral for a derivatives position. The bank now has to determine eligibility, contact custodians, verify valuations, move the T-bills, and wait for confirmations. Usually, it takes one to two business days before the collateral finally reaches the place where it can be used.

Tokenized collateral, however, can be moved in minutes or even seconds, with automated checks and compliance replacing days of waiting for traditional workflows.

This is especially important during periods of market stress and volatility, when collateral is needed most to reduce risk. Under the traditional workflow, risk continues to grow while market participants wait for their collateral to be deployed. With tokenization, assets can move where they are needed within minutes.

The ability to move collateral quickly could reduce liquidity buffers and improve capital efficiency. A study by GMFA states that a global bank with $100B in daily repo volume can save $150-300M annually by improving collateral usage efficiency. Scaled to the U.S. repo market, with roughly $10T in daily volume, that translates to $15-30 billion in annual savings.

The actual impact may be even greater, as institutions would have more opportunities to deploy their capital without increasing risk. This explains why BlackRock, JPMorgan, Goldman Sachs, and dozens of the world’s largest financial institutions are participating in the AppChain’s development and testing: they want it launched to reduce costs and unlock new opportunities.

How the Chainlink Tokenization Pilot with DTCC Makes the Difference

It’s false to think that all collateral-related processes are done manually. Large banks already have their own collateral management systems that automate margin and collateral processes. However, those systems are fragmented and lack a shared layer.

So, when Bank A tries to increase the collateral for its margin position, it’s communicating with Banks B, C, D, and E, and the whole operation depends on their responses. Sometimes communication is impossible, so the collateral gets trapped within certain regions or products.

DTCC saw the solution in a shared layer that would keep collateral-related data available to all participants — the AppChain.

The AppChain is meant to support tokenized securities, stablecoins, money market funds, and a variety of other assets, including crypto. Institutions bring an asset into the system along with its tokenized equivalent so it can be tracked and moved on the AppChain.

Each asset type requires a separate smart contract with unique rules attached to it, for example, to restrict usage in certain jurisdictions or to enforce eligibility under specific conditions.

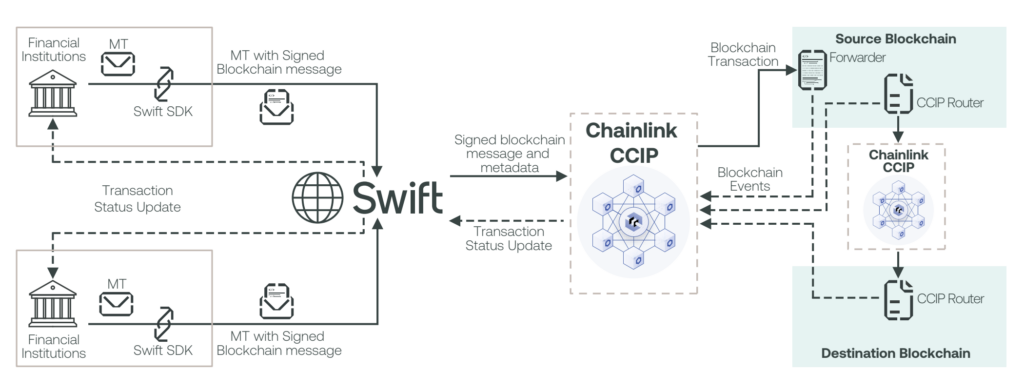

Then, tokenized assets need data. DTCC chose Chainlink to provide the AppChain with an asset’s current price, valuation, margining, and settlement through Chainlink Runtime Environment and Data Feeds. CRE orchestrates the process: when an asset is posted as collateral, CRE manages eligibility checks, data fetching, and calculations, then moves it to settlement. The receiving side gets a verifiable update that the collateral has been allocated. DTCC stated that tokenized collateral deployment took seconds, while the traditional workflow required at least several hours for the receiving side to receive settlement confirmation.

The interesting part is that banks and institutions don’t need to abandon fiat money or other traditional assets. The AppChain gives them an additional shared infrastructure to move collateral in seconds without replacing traditional tools.

What Success Would Mean

Launching the AppChain with full-fledged tokenized collateral management on a shared layer across major institutions would lead to increased collateral mobility and improved capital efficiency. This could also enable the creation of continuous markets: the AppChain can operate 24/7, allowing participants to manage their collateral outside local market hours instead of waiting for the next settlement cycle.

There would also be clear benefits for Chainlink:

- Generating recurring demand for its services. Collateral solutions require frequent data updates, which would be delivered by Chainlink and paid for in the LINK token.

- Becoming a recognized financial infrastructure provider. This is important because many people still associate Chainlink only with DeFi price feeds.

- Setting standards for finance. Institutions adopting DTCC’s infrastructure will also be adopting Chainlink’s standards, giving the industry a strong incentive to use both those standards and Chainlink’s services in other areas suitable for tokenization, such as repo transactions, securities lending, fund subscriptions, bond issuance, tokenized deposits, and more.

For the broader industry, the effects of tokenization will become visible over a longer time frame. DTCC’s roadmap is conservative: in 2024-2025, it proved the technology; in 2026, it built and tested Chainlink-powered infrastructure with plans to go into production in Q4 2026, then expand the list of collateral assets eligible for tokenization to increase adoption.

Conclusions

DTCC’s Collateral AppChain is a bold step in the evolution of the global financial system. Digital assets are superior to traditional, centralized, fragmented databases, and DTCC is about to prove it.

The AppChain might become Chainlink’s biggest use case to date because of the important role Chainlink plays in it, the more than $200T of assets it could eventually support, and the participation of the world’s largest financial institutions in its development and testing.

For Chainlink, it’s an opportunity to turn the brand into a seal of quality, signaling that if a financial product has Chainlink underneath, it’s probably built by the world’s leading institutions for the world’s leading institutions. That’s why we think the Collateral AppChain is Chainlink’s biggest use case yet.

.png)

.jpg)

.webp)